Why Late Fees Don’t Work

Late fees sound like a smart way to encourage customers to pay on time. On paper, the logic makes sense: if a customer knows there is a penalty for paying late, they should be more motivated to pay quickly.

In reality, that is rarely what happens.

For small and mid-sized businesses, late fees often create the illusion of action without actually solving the real problem. They do not create real urgency, they do not meaningfully protect cash flow, and they can quietly cost a business far more than they ever recover.

The bigger issue is not the fee. It is the aging invoice.

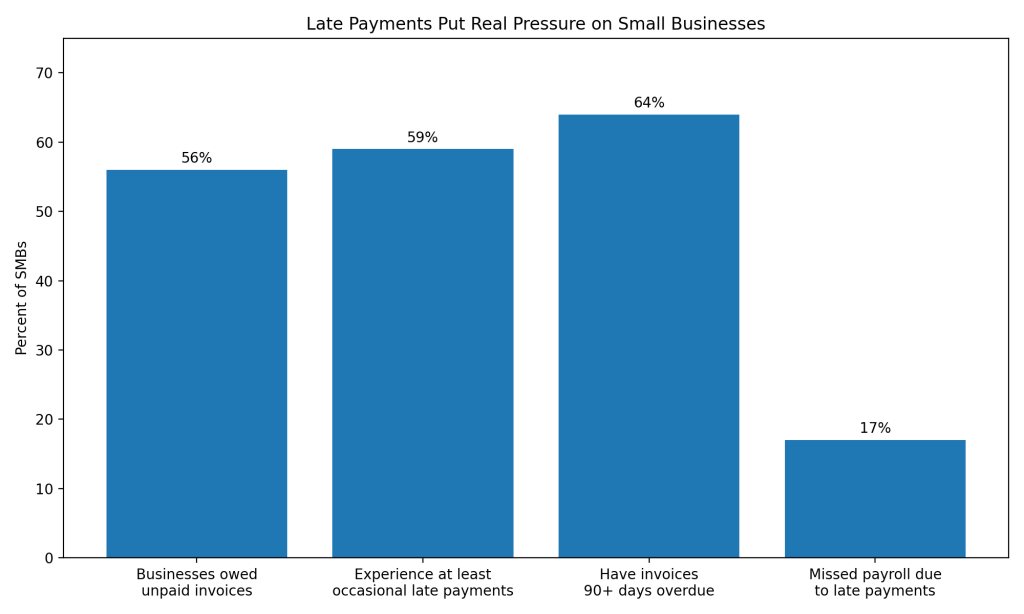

Recent small-business data shows that 56% of U.S. small businesses are owed money from unpaid invoices, with the average affected business owed about $17,500. Another 59% of small businesses experience at least occasional late payments, and 64% report having invoices that are 90 days overdue or more. That is not a minor inconvenience. It is a cash-flow problem that can slow growth, create stress, and force businesses into reactive decisions.

Late payments are a major cash-flow problem for SMBs

Small businesses do not usually fail because revenue never existed. They struggle because earned revenue does not arrive when it is supposed to.

When invoices are paid late, the business still has to cover payroll, rent, software, inventory, vendors, taxes, and every other normal operating cost. That gap between money earned and money received is where cash flow gets squeezed.

What makes this especially serious is the operational impact. Bluevine reports that 17% of small business owners have missed payroll because of late payments, and nearly 3 in 10 have delayed paying themselves.

That means late payments do not stay in accounting. They spread into hiring, owner compensation, vendor relationships, and growth planning.

Why late fees are usually ineffective

The biggest weakness of late fees is simple: they do not make your invoice a priority.

If a customer has already delayed paying you, adding a 1.5% or 2% fee usually does not suddenly change their behavior. In many cases, the customer will ignore the fee, dispute it, or continue delaying payment.

That means the business spends more time chasing the invoice while the receivable continues to age.

A late fee may look good in a contract, but it often does very little in the real world when a customer is already deprioritizing payment.

The hidden cost of waiting

This is where businesses lose real money.

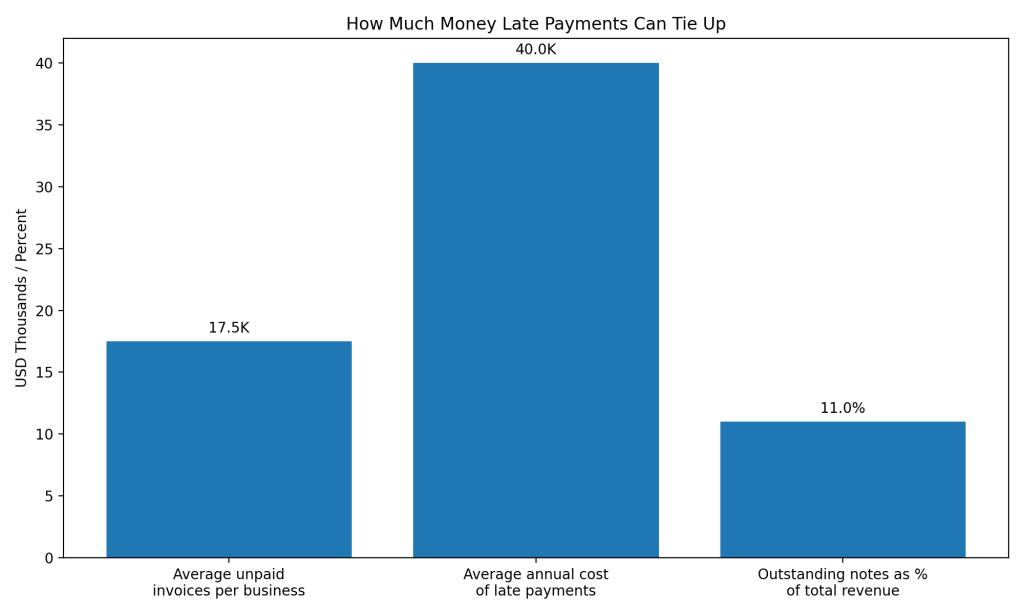

According to the QuickBooks late-payments report, affected small businesses are owed about $17,500 on average, while Old National cites survey findings showing the amount tied up in outstanding notes equals about 11% of total revenue on average. Kaplan’s roundup of payment-delay research puts the average annual cost of late payments at about $39,406 per company, and Old National rounds that to about $40,000 annually.

This is the part many businesses miss: late fees focus attention on a small penalty, while the real risk is the growing chance that the business will not recover the invoice in full.

Example:

If your business is owed a $10,000 invoice and your late fee is 2%, that adds only $200.

But if the account keeps aging and turns into a major collection problem, the business is not really fighting over $200. It is fighting over whether it gets the $10,000 back at all.

That is the trap. Late fees make businesses focus on pennies while they lose dollars.

A late fee is tiny compared with the cash at risk

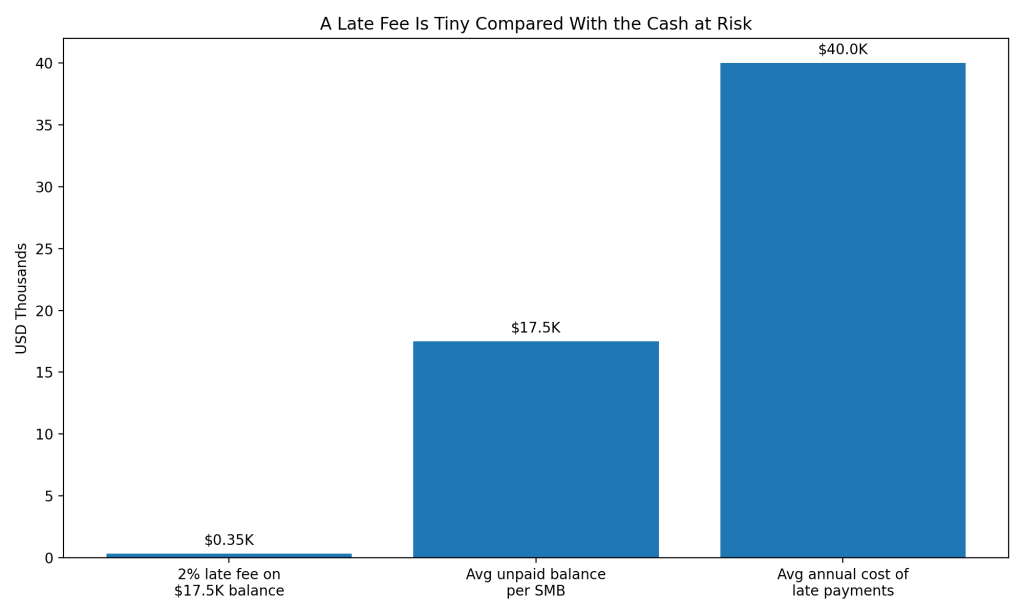

Using the current QuickBooks average unpaid balance of $17,500, a 2% late fee would equal just $350. That is tiny compared with the size of the receivable itself, and tiny compared with the roughly $39,000 to $40,000 annual costbusinesses report from late payments. The comparison below is partly illustrative, but it makes the core point clearly: the fee is small; the cash-flow damage is not.

Late fees can also damage customer relationships

Late fees are often intended to create accountability, but they can also create friction.

Instead of prompting payment, they may lead to:

- arguments over billing terms

- customer dissatisfaction

- more excuses and delays

- strained business relationships

For many B2B companies, preserving the relationship still matters. A tactic that creates conflict without meaningfully improving collections is not a strong long-term answer.

The real cost of late payments for small businesses

Let’s put this in practical terms.

If an SMB generates $1 million in annual revenue and roughly 11% of revenue is tied up in outstanding receivables, that means about $110,000 is sitting out in the market. If a meaningful share of that becomes delayed, disputed, or uncollectible, the business is not just dealing with a bookkeeping nuisance. It is losing working capital that should have funded payroll, hiring, inventory, marketing, or growth. The 11% figure here comes from survey reporting summarized by Old National.

That is why this issue is so serious. It is not just about accounting. It affects the entire business.

What works better than late fees

The businesses that protect cash flow most effectively are not the ones with the harshest late fees. They are the ones that take action earlier.

That means:

- addressing overdue invoices before they become severely aged

- creating accountability earlier in the collection cycle

- using a structured recovery process instead of passive penalties

- treating aging receivables as a cash-flow priority, not just an accounting issue

The sooner a business acts, the more control it has over the outcome.

Why this matters for Validate

This is exactly where Validate creates value.

Instead of waiting 60, 90, or more days and hoping a late fee changes customer behavior, businesses can act earlier and create real urgency before the receivable becomes a write-off.

Validate helps businesses move beyond passive tactics and toward a smarter, faster recovery approach.

That means:

- faster action

- better recovery outcomes

- less cash-flow disruption

- fewer write-offs

- more control over revenue that has already been earned

Final takeaway

Late fees may feel like a solution, but for most SMBs, they do not solve the real problem.

They do not create meaningful urgency. They do not improve cash flow in a major way. And they do not prevent the much larger financial damage caused by aging receivables.

The real cost is not the fee.

The real cost is the revenue your business may never recover because it waited too long to act.

If your business is serious about cash flow, growth, and protecting earned revenue, it is time to move beyond late fees and focus on early recovery.

Take control of your cash flow

If unpaid invoices are slowing down your business, Validate can help you take action earlier and recover revenue before it turns into bad debt.

When customers don’t pay, Validate is the way.

Late Fee FAQ:

Do late fees actually help small businesses get paid faster?

Usually not by much. Late fees may create a contractual penalty, but they often do not make the invoice a real priority for the customer. Earlier intervention is usually more effective.

How much do late payments cost small businesses?

Recent reporting puts the average annual cost of late payments at roughly $39,000 to $40,000 per business, with affected small businesses owed about $17,500 on average in unpaid invoices.

How common are unpaid invoices for small businesses?

Very common. QuickBooks reports that 56% of U.S. small businesses are owed money from unpaid invoices, and Bluevine reports that 59% experience at least occasional late payments.

Why are late payments so dangerous for cash flow?

Because expenses keep moving even when receivables do not. Payroll, rent, software, and vendors still have to be paid, so slow invoices create pressure across the business.

Sources

- Intuit QuickBooks, 2025 US Small Business Late Payments Report

- Bluevine, 2026 survey findings on late payments and payroll impact

- Old National, Unpaid Customer Invoices Are Piling Up, Squeezing Small Businesses

- Kaplan Collection Agency, Statistics on B2B Payment Delays